Long Term Care Insurance Policy

Frequently Asked Questions

Long Term Care FAQs

Click the questions below to learn more about long term care FAQs. I’m available anytime to discuss your needs or answer any additional questions you might have.

What is Long Term Care?

Long term care is the type of care you may need if you have a prolonged physical illness, disability or cognitive impairment (such as Alzheimer’s disease) that keeps you from living independently. These limitations may prevent you from carrying out basic self-care tasks – such as bathing, dressing, or eating – called Activities of Daily Living (ADLs).

Even if you think that you may never require extended care, the financial, physical and emotional consequences are so significant that they really need to be addressed.

About 70% of people over age 65 require some type of long term care services during their lifetime.1

What is a Hybrid Long Term Care Insurance Policy?

“Live, Die or Quit” is the motto of a hybrid LTC policy. If someone lives a long life and does need extended care, it’s addressed. If that person passes away without needing care, that’s addressed as well. Or, if the person decides to give up the plan and receive funds back, that’s also an included feature of the policy.

Hybrid life/LTC insurance combines the benefits of life insurance with long term care benefits. There are also hybrid annuity/LTC policy options that combine an annuity with long term care protection. The following information refers to hybrid life/LTC policies.

Hybrid life/LTC premiums may be paid as a one-time lump sum payment, or as annual payments over a number of years.

If the policyholder needs long term care, the policy will pay benefits for those expenses, including home care expenses. Similar to a traditional LTC policy, the benefits are paid in an amount chosen when the policy is purchased and are often expressed as an amount per month. Inflation protection can often be added to help ensure that the LTC benefit keeps pace with future costs.

If a policyholder passes away without needing care, there is a tax-free death benefit paid to beneficiaries which is at least equal to the amount paid into the policy. Therefore the policy owner can rest assured that money spent for long term care insurance would not be have been “wasted”.

However, if long term care is needed, the amount of money available for care will greatly exceed the death benefit, offering tremendous leverage of premium dollars. And the premium paid into the policy is guaranteed not to increase.

If someone had earmarked $100,000 for an investment account for future LTC needs, but instead used that $100,000 to purchase a hybrid life/LTC policy, the potential LTC benefits paid out could be at least $400,000 depending on many factors. Thus, there is significant leverage available in placing that sum of money in the policy instead of investing the premiums and “self-insuring”.

Hybrid life/LTC policies have opened up new ways of thinking about the role of LTC protection within a person’s overall estate and financial plans. Because of their unique characteristics, these policies can be popular with people who may be unsure if traditional LTC insurance is right for them.

Types of Long Term Care

Homemaker Services and Home Health Aides

This service provides care that allows people to live in their own homes or to return to their homes by helping complete household tasks they can’t manage alone. Homemaker services aides may clean houses, cook meals or run errands. Often they are referred to as “Personal Care Assistants” or “Companions.”

This service provides care that allows people to live in their own homes or to return to their homes by helping complete household tasks they can’t manage alone. Homemaker services aides may clean houses, cook meals or run errands. Often they are referred to as “Personal Care Assistants” or “Companions.”

Personal and home health aides provide “hands-on” personal care, but not medical care, in the home with activities such as bathing, dressing and transferring. This service provides assistance to those who are elderly, disabled or too ill to live in their own homes or in residential care facilities instead of in nursing homes. Home health aides may offer care to people who need more extensive personal care than family or friends are able to, or have the time or resources to provide.

Adult Day Health Care (ADH)

Adult Day Health Care centers can offer a much-needed break to caregivers. This type of care provides service at a community-based center in a protective setting for adults who need assistance or supervision during the day but who do not need around-the-clock care. Some programs also may provide personal care, transportation, medication management, health-related services, inter-generational programming, social services, meals, personal assistance, and therapeutic activities.

Assisted Living Facilities (ALF)

Assisted living facilities are living arrangements that provide “hands-on” personal care and health services for people who may need assistance with ADLs, but who wish to live as independently as possible and who do not need the level of care provided by a nursing home. It’s important to note that assisted living is not an alternative to a nursing home, but an intermediate level of long term care.

Nursing Home Care

Nursing homes are for those people who may need a higher level of supervision and care than in an assisted living facility. They offer residents personal care, room and board, supervision, medication, therapies and rehabilitation, as well as skilled nursing care 24 hours a day.

What Does Long Term Care Cost in the U.S.?

According to Genworth Financial’s 2025 Cost of Care Survey conducted by CareScout®, here are the median rates in 2025 for the following types of care in the U.S. However, there are significant variances between states and even between geographic areas within the same state.

National Rates 2025

- Home Health Aide – $35 per hour

- Adult Day Health Care – $95 per day

- Assisted Living Facility – $204 per day

- Nursing Home Private Room – $355 per day

Rates in the Boston, MA area (where I live)

- Home Health Aide – $41 per hour

- Adult Day Health Care – $112 per day

- Assisted Living Facility – $317 per day

- Nursing Home Private Room – $510 per day

Click here for interactive information by state for detailed costs today and in the future.

The cost of care for assisted living facilities and nursing homes has increased between 7-10% per year over the past five years, depending on the type of facility.

How well will your retirement portfolio cover these expenses when you are elderly?

If one spouse needed care, what would the financial impact be on the other healthy spouse?

Doesn't Medicare and Medicaid Pay for Long Term Care?

Medicare

Generally, Medicare is the federal program that:

- Provides hospital and medical insurance to people aged 65 or older and to certain ill or disabled persons.

- Limited benefits that may be available for skilled, brief home health care visits if certain conditions are met.

- May pay for up to 100 days of care in a skilled nursing facility per benefit period – 100% for the first 20 days (after a three-day hospital stay, provided skilled care is needed). Then, for days 21-100, Medicare requires a co-payment. To help cover the co-payment, many people 65 and older also have a Medicare supplement insurance policy. Learn more about this coverage at Medicare.gov.

Medicaid

- Medicaid generally pays for certain health services and nursing home care for those with low incomes and limited resources. Medicaid has limitations on the amount of assets you can own and the amount of income you may receive each month before you are eligible for benefits. Who is eligible and what services are covered vary from state to state. There are also restrictions on transferring assets to others in order to qualify for Medicaid.

- Medicaid coverage of Nursing Facility Services is available only for services provided in a nursing home licensed and certified by the state survey agency as a Medicaid Nursing Facility.

Not intended as legal advice. Consult an attorney for details.

Long Term Care Insurance: Weighing the Options

The cost of Long Term Care Insurance premiums is largely dependent on several factors, including age, policy type, and level of coverage (nursing home vs. in-home or assisted-living care or another type of care). Therefore, it is always smarter to purchase a policy while you are younger and healthier since coverage will always be less expensive and easier to meet health qualifications.

Hybrid insurance products that include a death benefit are also worth exploring for many people. These hybrid policies address the following questions:

- What if I do require long term care – are there sufficient funds to cover the cost of that care?

- What if I don’t need care…what happens to the premiums I have already paid into the policy?

- What if I change my mind and want to “cash in” the policy?

For further information please see the “What is a Hybrid?” section above.

Having a plan in place to address extended care can provide these benefits:

- Keeping financial commitments during retirement

- Securing the financial viability of the other spouse

- Potentially reducing taxes by avoiding selling an asset that would involve capital gains

- Potentially avoiding the need to sell assets during a down market in order to fund care

If you have no assets and don’t have the income to afford long term care insurance, you might be eligible for Medicaid. In this case, long term care insurance might not be right for you. But for many Americans, a sensible policy purchased at a relatively young age can be one of the smartest retirement-planning moves one can make.

Shopping Tips

Long term care insurance does not have to be as expensive as you may have thought. There are many options that can be customized to meet your needs and budget. It’s a good idea to compare policies from several companies, but this process can be confusing. Covered services can vary among insurers.

Considerations in researching long term care insurance policies:

- Is it a tax-qualified policy?

- What is the appropriate daily or monthly benefit?

- How long will the benefits last?

- Is there built-in inflation protection?

- What is the Elimination Period (similar to a waiting period or a deductible)?

- Is 100% of the benefit available for home care?

- Are there any riders that might be appropriate?

- Is the policy guaranteed to be renewable?

- What conditions must be met to collect benefits?

- What types of facilities are covered?

- Will the policy pay for custodial, or personal, home care or hospice care?

- What happens if your policy lapses after you’ve paid premiums for many years?

- Will the policy pay expenses outside of your local area?

Can I use my IRA to pay for LTC insurance?

Yes! You can use funds from both Traditional and Roth IRAs to pay for qualified long-term care insurance premiums, and this is often a smart strategy that many people overlook.

Traditional IRA: If you’re age 59½ or older, you can use money from a traditional IRA to help pay for long-term care insurance without facing the IRS early-withdrawal penalty. However, the amount you withdraw will still be taxed as ordinary income, since traditional IRAs are funded with pre-tax dollars. There’s no special tax break just because the money is used for long-term care insurance, but many people choose this strategy once they’re past age 59½ because it provides flexibility and avoids penalties. It’s important to note that even though the withdrawal is penalty-free,know that it can increase your taxable income for the year.

Roth IRA: With a Roth IRA, you can withdraw your contributions tax-free at any time and at any age since you’ve already paid taxes on that money. Earnings (growth, interest, gains) also come out tax-free as long as you’re at least 59½ AND your first Roth contribution was made at least 5 years ago. A Roth IRA can be particularly attractive for funding long-term care protection.

What about hybrid policies? Many of my clients have used IRA funds for a direct transfer into a hybrid long-term care policy (also called asset-based LTC insurance). With a hybrid policy, life insurance or an annuity is combined with long-term care benefits. This is particularly popular because:

- Your money isn’t “use it or lose it”—if you never need care, your beneficiaries receive the unused proceeds in the form of a death benefit for the life insurance policy, or the Account Value for the annuity

- You can often fund it with a single premium payment directly from your IRA

- There are no ongoing monthly premiums to worry about in retirement

Why this matters: Many retirees are sitting on substantial IRA balances but worry about monthly cash flow for insurance premiums. Using your IRA strategically can help you protect your other retirement assets from the devastating cost of long-term care, which averages $108,000+ annually for nursing home care.

Important note: Every financial situation is unique. I recommend consulting with both a tax advisor and a financial planner to determine the best strategy for your specific circumstances. I’m happy to coordinate with your other advisors to ensure your long-term care plan works seamlessly with your overall retirement strategy.

Can I deduct a long term care insurance premium?

Long Term Care Insurance Premium Deductions for the Self-Employed

If you’re self-employed, you may be able to deduct qualified long-term care insurance premiums as a business expense, which is more advantageous than the standard medical expense deduction available to W-2 employees.

Key advantages for the self-employed:

Self-employed individuals can deduct qualified LTC insurance premiums on Schedule 1 (Form 1040) as part of the self-employed health insurance deduction. This is an “above-the-line” deduction, meaning you don’t need to itemize to claim it, and it’s not subject to the 7.5% of AGI threshold that applies to medical expense deductions.

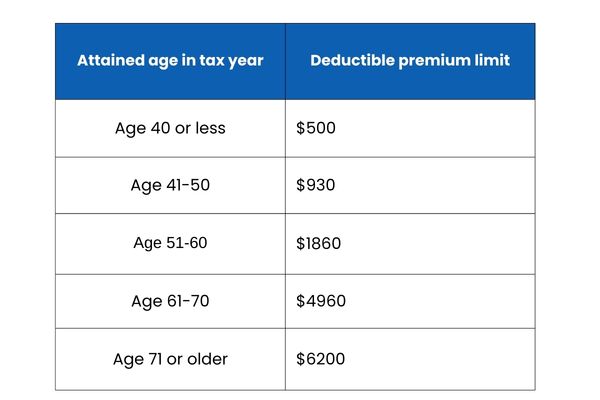

Important limitations:

The deductible amount is limited by age-based maximums set annually by the IRS (see 2026 chart below). You can only deduct premiums up to these limits, even if your actual premium is higher. Additionally, your total self-employed health insurance deduction cannot exceed your net self-employment income for the year.

Who qualifies:

This applies to sole proprietors, partners, and more-than-2% S corporation shareholders who have a net profit from self-employment and aren’t eligible to participate in an employer-subsidized health plan through a spouse’s employer.

Note: Please consult with your tax advisor.

“Meredith Pensack is by far the best insurance specialist I have ever worked with. She not only is incredibly knowledgeable about competing products, but also was able to distill and communicate the subtle but important differences in the products so that I could make the absolute right decision about price and coverage that best met my needs. When faced with obstacles she never, ever gave up, but worked with me and the insurance companies for more than one year until I was approved for the policy that I both deserved and desired. I have recommended her to others who have benefited from her experience and professionalism. This is one person that I always want on my side.” – J.L.

Request a Quote or Contact Me

By Completing the Information Below

"*" indicates required fields